If you’re a business owner in Ireland with surplus cash on your balance sheet, you might believe the bank is the safest place for it. However, in the current financial climate, it may be time to rethink that age-old wisdom. The European Central Bank (ECB) has been pushing interest rates up all year, but traditional Irish banks are still not offering much of a return to savers. Why is this the case, and what can you do about it?

How ECB rate changes impact your business savings in Ireland

For years, savers endured pitiful returns on their deposits as interest rates were kept low to encourage economic activity. You’d expect that recently rising ECB interest rates and inflation would have combined to turn back the tide, but unfortunately that’s not really the case in Ireland. While the banks have been quick to pass these hikes onto borrowers, those with cash deposits are still stuck in the doldrums.

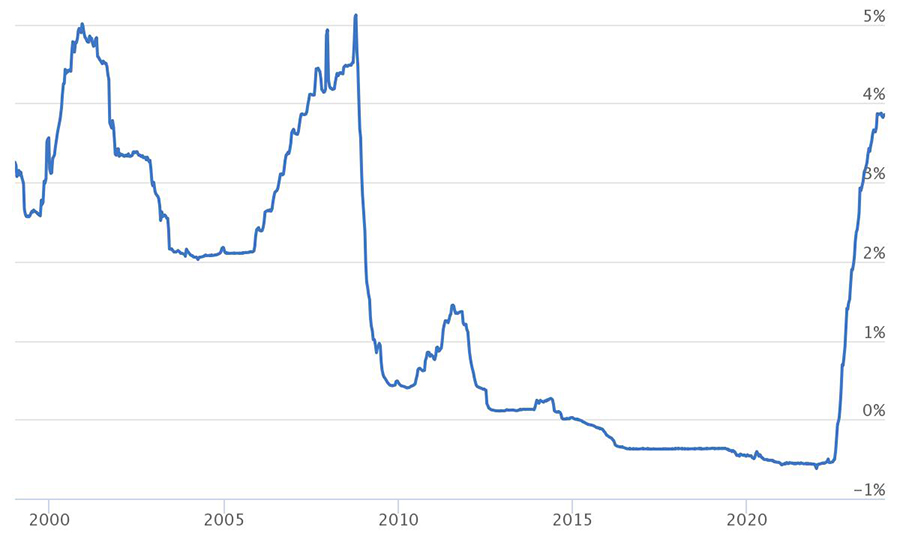

In Ireland, traditional banks are still offering paltry interest rates on business deposits. The ECB deposit facility rate is at an all-time high of 4%, and climbing, but our banks are barely offering half that – if you’re lucky. Inflation rates are at levels not seen since the 1970s, meaning the purchasing power of your surplus cash is actually dwindling as it sits in the bank. For people like me and you, it’s grating to see these bailed-out banks now earning substantial margins by themselves placing their cash on deposit with the ECB.

Life is great if you’re an Irish bank. Both Bank of Ireland and Allied Irish banks reported pre-tax profits of over €1 billion for the first six months of this year, and a big driver of that is their net interest income. BOI’s rose 68% in the first half of 2023 compared to 2022, to €1.8 billion. How? It can make over €1 billion in annual interest by parking €29 billion of our money with the European Central Bank. Learn more in the David McWilliams podcast episode, The Easiest Way to Rob a Bank is to Run It.

But while banks turn a more than tidy profit, your hard-earned cash is not working as hard as it could be. For businesses that have done well and built up a cash surplus, it’s essential to protect the value of that cash so that it’s there for future investments, expenses, opportunities, or dividends. As directors, we have a fiduciary responsibility to manage our business assets wisely for the benefit of shareholders. But we don’t have a lot of options available to us in this market.

The hidden risks of storing business surplus cash in Irish banks

Given low saver rates and the shifting banking landscape more generally, are banks even the best place for our money these days? In Ireland, the Deposit Guarantee Schemes (DGS) only protects deposits up to €100,000 (for individuals and most SMEs). If you have a significant amount of surplus funds, you’re taking a gamble that goes beyond mere interest rates. Let’s not forget that these banks have a chequered history and needed bailouts in the not-distant past. Putting all your eggs in one basket, especially a basket that’s been shown to have holes, might not be the wisest move.

Another overlooked risk is the opportunity cost. With your money languishing in a low-interest account, you’re missing out on other investment avenues that could offer better returns. In a business landscape where every euro counts, that could mean the difference between expanding your operations or maintaining the status quo. Efficiently managed cash can grow through strategic investment, contributing to the overall value of the company.

A practical alternative: investing with Zurich Life

If you’ve been grappling with the dilemma of where to park your surplus funds, we have some first-hand experience to share. We also faced this issue and decided to investigate whether there were alternatives that could provide us with better returns than the traditional banking system.

As we already had a relationship with Zurich Life, we put the question to them. They told us that as well as their core, primarily equity-based funds for long-term pension planning, they have lower-risk funds and/or government bonds where the focus is on cash. These products had lost their popularity but have been coming back into favour because of the recent increases in rates at the large international banks used by Zurich Life.

As it turns out, Zurich Life – like Irish Life or Aviva and other big players in the market – offers investment options that are particularly suitable for company funds in our current economic climate. Unlike the grim interest rates offered on cash deposits by Irish banks, Zurich Life’s offerings look rather attractive. I even recorded a conversation with David Walls, Head of Investment Sales at Zurich, covering the kinds of questions our clients might have about this.

What’s on offer?

Zurich Life has a range of investment options that cater to different risk profiles, from the cautious to the more adventurous. The one that caught our attention was the Zurich Life Cash Fund. Unlike a deposit account, this fund combines overnight deposits, term deposits, and short-term European Government bonds.

The recent upturn in interest rates has made this fund particularly appealing, offering a current yield of around 3.5% (before charges and with some fluctuation in value due to the bond component). As far as annualised returns are concerned, the year-to-date figure stands at a respectable 2.1%, which equates to about 2.9% annualised.

How long is the money tied up?

Investment bonds like those offered by Zurich Life typically have varying terms and conditions. While they are generally considered medium- to long-term investments, Zurich Life Investment bonds offer options for early withdrawal. If you need access to your money, there are options available that allow you to release it within a few weeks. I took a three-to-five-year view of our investment, which I think is the right kind of timeframe to have in mind.

What is the tax liability on interest?

If you’re concerned about the tax implications, you’ll be pleased to hear that company funds can benefit from a special corporate tax rate of 25% on returns (gains), as opposed to the 41% rate for individuals.

How do you go about this?

If your business has cash reserves that it isn’t likely to need for now, a cash fund is a possible solution. We can walk through this with you and look at the options available to pick the best one. The process itself isn’t too onerous. There are a few anti-money lending hoops to jump through, but we will handle the paperwork for you. It typically takes a few days to a couple of weeks to get up and running if the application is straightforward.

Keeping an eye on your investment is easy, thanks to Zurich’s user-friendly online platform and mobile app. You can log into the online Client Centre or use the app to view real-time updates on your fund’s performance. The platform also comes equipped with a range of handy tools, calculators, and informative videos. This means you’ll have everything you need at your fingertips to stay fully informed about your investment. It’s a transparent and accessible way to monitor how your money is working for you.

Moving away from traditional banking

We’ve already taken the plunge and invested our own surplus funds in a low-risk cash fund. If you have surplus cash, you might find that it’s worth stepping out of the traditional banking market and into an alternative ecosystem that offers greater returns without compromising much on risk or liquidity.

I certainly feel it’s a wiser approach to work with a respected and trusted partner like Zurich Life than to go knocking on the door of some unknown private equity firm. Remember, investment products come with risk ratings (ranging from 2 to 7) so that people understand the potential volatility and level of risk associated. This allows you to align your choices with your risk tolerance and financial goals.

If you would like to discuss moving your cash reserves out of your bank’s deposit account, get in touch to set up a meeting with me.

N.B. If you purchase a Zurich Life product based on a recommendation from Beyond Accounting, we will receive a small commission that comes directly from Zurich Life and is not taken from your investment.

If sound financial management is a priority for your business, you might benefit from an outsourced accounting package from Beyond. We look after the day-to-day, but also have an eye on your longer-term strategy and growth plans. Get in contact with us today to see how we could help.

Rory

P.S. If you find our articles informative, you can add us to your preferred Google search sources.