If current trends continue, the days of paying for goods and services with cash or a cheque will become just another story we tell our incredulous grandchildren. The payments sector continues to evolve, and it’s important that businesses are aware of what is available in the market as well as what will become possible tomorrow.

The changing payments landscape

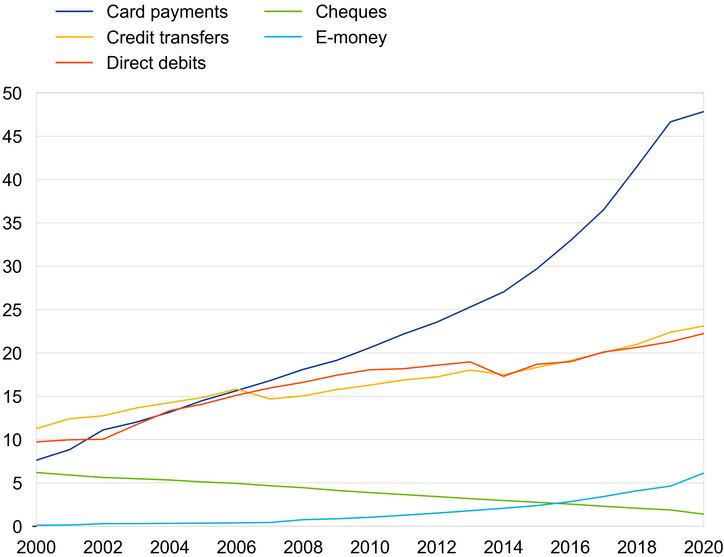

As of the most recent figures (2020), non-cash transactions in the zone amounted to €167.3 trillion. Europeans possess an average of 1.8 cards with a payment function and there are 12.2 million physical point of sale (POS) terminals in use. Mobile and contactless payments are growing in popularity too. Commerce businesses that resisted going digital have had the past two years to reconsider their choices, and many have played catchup as consumers voted with their (virtual) wallets.

Use of the main payment services in the euro area (number of transactions per year in billions)

Across the world, fintechs are inventing and reinventing payments methods, and here in Europe their job is being made a little easier thanks to Open Banking and the EU’s Payment Services Directive (PSD2). Often, though, the underlying infrastructure they are building on remains unchanged (the MasterCard and Visa networks, for example). So, we are likely to see completely new models emerging in terms of infrastructure too.

It’s all something of an existential threat to traditional banks. Here in Ireland, AIB, Bank of Ireland, KBC Ireland, and Permanent TSB came together during the pandemic to create their own mobile payments service, Yippay. With a reported development pot of €11 million, it was hoped the platform would enable them to compete with digital operators such as Revolut and N26. These plans have stalled at present due to an investigation by the Competition and Consumer Protection Commission (CCPC), which should be published in 2022.

Are your payment solutions meeting customer needs?

What does this mean for your business? If you’re still relying on EFTs and merchant/ecommerce services from a traditional domestic bank like BOI or AIB, it could well be worth looking at the alternatives, of which there are now many. These challenger services tend to have a much better user experience (for you and your customers) and lower fees. If your business involves a lot of transactions – whether B2B or B2C, incoming or outgoing – take some time to analyse their makeup and research the services out there to compare how each one could work for you. They all have their own ways of setting fees, so which one is best for you will really depend. Remember there could be:

- Regular maintenance fees/subscriptions

- Percentage fees on transactions

- Additional flat fees on transactions

- Currency exchange fees

- Withdrawal fees

Other factors that could affect your choice are the availability of apps (iOS, Android, desktop, etc.), the user interface, additional features, and the availability/quality of customer support.

Three ways to align with changing money habits

1. Make sure you’re offering the best ecommerce payment options

PayPal is not the only way to accept payments on your website (digital payments). Stripe is the biggest challenger to PayPal and offers better fee rates as well as a focus on the development side of payments (API, etc.). Also available in Europe are services such as Adyen, Square, BlueSnap, and Checkout.com. These providers typically support country-specific requirements too, such as the widespread use of ecommerce payment method iDEAL in the Netherlands and the mobile payment app Vipp, used in Norway. These are vital considerations if you are trying to grow in other markets.

Accepting card payments is great for business, but you are paying on average somewhere between 1.5% – 4% in fees no matter which payment gateway service you go for. Part of this is the bank interchange fee (the fee charged by banks to the merchant who processes a credit card or debit card payment) which changes from country to country. But it’s also because the transaction itself requires so many steps – the customer, the payment gateway, the card network, the payment processor, your bank, you, and the customer’s bank.

That’s why there is now so much interest in developing ways to accept digital payments without people needing a credit or debit card.

2. Look at alternatives to credit cards and debit cards

Between them, Visa and MasterCard control 90% of the credit and debit card market. Challenger banks like Starling, Revolut and N26 – while being attractive because of their better user experience – are still relying on this network as part of their business model. So, what’s the alternative? Peer-to-peer (P2P) and account-to-account (A2A) solutions bypass the Visa/MasterCard network entirely. Some of the players in this market include GoCardless, Melio, Banked, Libeo, Trustly, and Token.

The humble QR code, which you may have thought was old news, also offers a potential solution for low-value transactions (but it isn’t secure enough to become a mainstream payment option). Bypassing card payments means faster settlement times and lower processing fees, but it also offers other opportunities such as Buy Now Pay Later.

3. Consider whether you could offer a Buy Now, Pay Later (BNPL) option

Fintechs spotted huge potential in turning old-fashioned sales financing on its head by bringing automated credit into the digital mainstream. Also known as Point-of-Sale (POS) credit or POS financing, it allows consumers to access instant, (mostly) interest-free credit at the checkout.

The merchant does pay a fee on every transaction, but this makes financial sense because typically a consumer will spend considerably more if they have access to credit. According to Kaleido Intelligence, the e-commerce spend in Europe via Buy Now Pay Later (BNPL) is projected to hit $347 billion by 2025. The biggest EU movers in this market are humm (previously Flexi-Fi), Klarna, Alma, Cashper, PayPal, Scalapay, Cofidis, and Ratepay.

A variation on BNPL is an instalment card. Rather than a consumer having multiple BNPL agreements with a range of providers, they could get a card for these payments and pay the total in instalments. Klarma has recently released such a product, but it seems likely that credit card companies won’t welcome this overlap and will come to market with their own competing offers.

Changing consumer behaviour in the payments sector

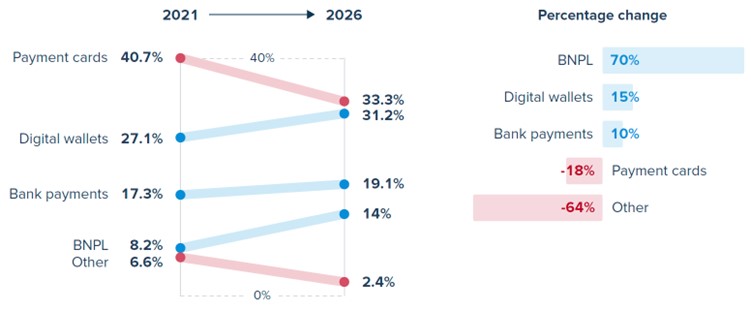

This analysis from TrueLayer (a fintech development platform) shows their predictions for the European ecommerce payments landscape from 2021 to 2026:

Businesses that want to optimise sales through high conversion rates should consider offering a broader range of payment options at checkout, so their customers can choose the payment method they prefer. Successive studies show that shoppers are more likely to buy when the ‘right’ payment option is available to them. A recent report from checkout.com, The new state of retail, shows that 80% of consumers expect to pay using new payment methods.

That’s why of 50% of European ecommerce merchants have responded to increased cross-border demand by expanding the range of alternative and local payment methods they offer since the start of the pandemic. The ecommerce businesses that address missed sales revenue and unnecessary payments costs in this way will be able to significantly improve turnover and profitability!

We make it our business to keep with all the latest developments in the retail/ecommerce sector so that we can help our clients grow and stay competitive. If you’d like to move to Beyond Accounting, get in contact today or call 01 639 2963.

Rory

P.S. If you find our articles informative, you can add us to your preferred Google search sources.